The Deterioration of Global Supply Chain Conditions

Global supply chain conditions continue to deteriorate, leading to operational risks according to CIPS risk index, powered by Dun & Bradstreet. By 24/7 Staff

March 11, 2016

Global supply chain risk increased in the fourth quarter of 2015, resuming the worsening trend in global operational risk according to the latest Chartered Institute of Procurement & Supply (CIPS) Risk Index, powered by Dun & Bradstreet.

The index’s high score reflects the general unease about the state of the global economy with its increase in operational risk and the Chinese slowdown highlighting emerging market vulnerabilities.

Key highlights from the index include:

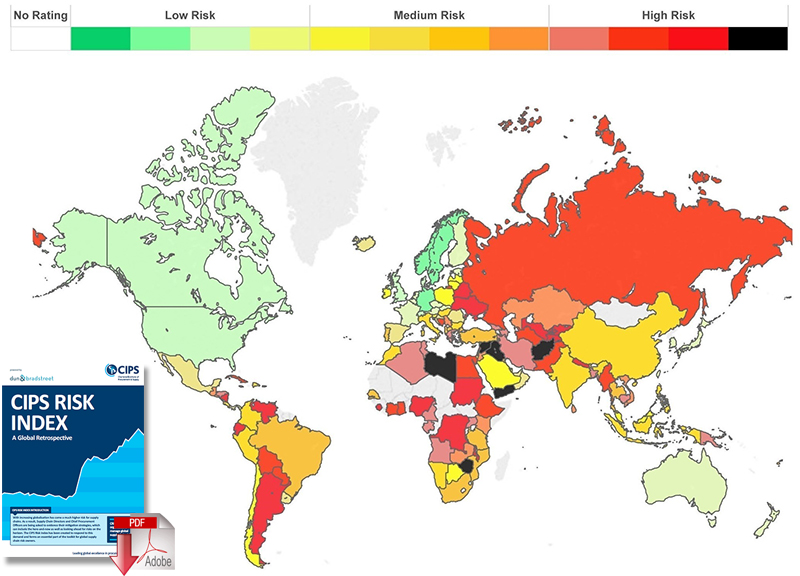

- Supply chain risk in Asia Pacific continued to rise due to worsening economic conditions in New Zealand, Australia and China.

- Sub-Saharan Africa’s supply chain risks fell slightly, though underlying risk trend continues to deteriorate.

- Though Iran’s re-entry into global supply chains encourages optimism, supply chain risk in the Middle East and North Africa (MENA) remains in the high risk category.

To determine the CIPS Risk Index, powered by Dun & Bradstreet, a Dun & Bradstreet team of in-house economists, data analysts and contributors analyzed 132 countries across nine risk and opportunity categories.*

The index score worsened slightly in the last quarter of 2015 to 79.3 from 79.1 in the third quarter of 2015. While some regions, including the EU, have improved since mid-2015, emerging markets now demonstrate more vulnerability.

Contribution to Global Supply Chain Risk in the Fourth Quarter Of 2015

Source: Dun & Bradstreet

Source: Dun & Bradstreet

Asia-Pacific’s Risk Increases Slightly Amid Negative External Impact From Shift In China’s Economic Outlook And Falling Commodity Prices

As Australia’s main trading partner, the slowdown in the Chinese economy and the resulting decline in demand for commodities has negatively impacted Australian suppliers. In China, risk is related to regions where industry has considerable over-capacity and local governments have propped up employment through their influence over local banks, raising both the risk of corporate defaults in the longer term, and higher credit risk.

As Australia’s main trading partner, the slowdown in the Chinese economy and the resulting decline in demand for commodities has negatively impacted Australian suppliers. In China, risk is related to regions where industry has considerable over-capacity and local governments have propped up employment through their influence over local banks, raising both the risk of corporate defaults in the longer term, and higher credit risk.

Supply chain risk was also increased in New Zealand, where Dun & Bradstreet downgraded the country risk outlook for the second time in 2015, driven by a 40% fall in global dairy prices (resulting in dairy prices reaching their lowest level since 2008). A too-slow recovery of prices in 2016 could result in a further decline in land prices (up to 10%) and an 8% rise in non-performing loans.

Sub-Saharan Africa Bucks Trend of Increased Risk, But Falling Global Commodity Prices Impact Region

Unlike many other regions, Sub-Saharan Africa saw a slight improvement in its score according to the CIPS Risk Index, powered by Dun & Bradstreet, as a result of improvements in Cote D’Ivoire, Namibia and Senegal.

Unlike many other regions, Sub-Saharan Africa saw a slight improvement in its score according to the CIPS Risk Index, powered by Dun & Bradstreet, as a result of improvements in Cote D’Ivoire, Namibia and Senegal.

These countries saw their Dun and Bradstreet country risk ratings upgraded due to diversification of their economies, commitments to invest in transportation and energy infrastructure and declining budget deficits.

Conversely, Malawi and Zambia’s country risk ratings were downgraded. Key challenges to Malawi include continued suspension of donor budgetary support due to a corruption scandal and weather-related challenges in the region. Zambia’s economy and risk have been negatively impacted by lower global commodity prices, particularly related to copper, and power shortages.

Though Experiencing a Marginal Improvement, MENA Supply Chain Risk Remains High; Re-Introduction of Iran to Global Supply Chain Encourages Optimism

Supply chain risk in MENA improved marginally in fourth quarter of 2015, but remained elevated by historical standards.

Supply chain risk in MENA improved marginally in fourth quarter of 2015, but remained elevated by historical standards.

The lifting of the sanctions on Iran should see the region benefit from new opportunities and assist regional and global supply chains in the medium term.

The increase in oil supply should keep energy prices low and in the short term negatively impact risk in oil exporting countries as government expenditure is cut.

These governments will need to create opportunities for cross-border trade and investment to see improvements in the medium term.

Egypt’s country risk rating was downgraded in the wake of the downing of a Russian airliner in Sinai which is having an impact on the tourism sector, an important source of employment and foreign exchange earnings. Throughout the region, the security situation is expected to keep risk at high levels through 2016 and into 2017.

John Glen, CIPS economist and director of Centre for Customized Executive Development said: “Though the overall index has virtually flat-lined the last quarter of 2015, no one should be fooled into thinking risk is reduced. Quite the opposite. The report shows continuing deterioration of risk conditions. Business leaders and supply chain professionals must be ever-vigilant and wary, placing both risk mitigation, and building supply chain resilience, to the top of their priority list.”

Oana Aristide, acting global leader and lead economist at Dun & Bradstreet, said: “The fourth quarter of 2015 was dominated by non-economic news, such as the Paris terror attacks and the continued refugee inflows into Europe, combined with the increased political resistance and sometimes controversial measures aimed at curtailing these inflows. While both of these have a limited impact in terms of disrupting business activity, they do affect investor and consumer confidence.

Meanwhile, the Federal Reserve lift-off and growth deceleration in China raised concerns about emerging markets’ vulnerabilities. The business uncertainty – a feature of the global economy since the end of the recession – continues to stifle consumer confidence, which is necessary for a robust global recovery.”

* Calculations of the CIPS Risk Index, powered by Dun & Bradstreet, is composed of multiple unique assessments undertaken by Dun & Bradstreet’s team of in-house economists, data analysts and contributors working in-field across the world. In all, 132 countries (comprising 90+% of global economic activity) are assessed across nine categories, on a monthly basis. The individual country scores are then aggregated to calculate a global supply risk score. The weights used for each country are based on the contribution each country makes to total global exports (in theory, their individual contribution to global supply chains). The trade shares are anchored to data for 2010 to facilitate consistent comparison of the index scores over time. The regional scores are done in the same way, aggregating across all countries in the region based on their contribution to total exports.

CIPS RISK INDEX A Global Retrospective

No comments:

Post a Comment