Older consumers: redefining health and wellness as they age

2017-06-06

The marketplace belongs to the older consumer. What? Really…it’s true. While marketers crave and court the 18-to-49 demographic, the world is actually getting older. We’re closing in on a milepost marker not seen in human history before: according to the U.S. Census Bureau as we get close to 2020, the number of people 65 and older will surpass those under 5 for the first time. And we’re living longer.

The marketplace belongs to the older consumer. What? Really…it’s true. While marketers crave and court the 18-to-49 demographic, the world is actually getting older. We’re closing in on a milepost marker not seen in human history before: according to the U.S. Census Bureau as we get close to 2020, the number of people 65 and older will surpass those under 5 for the first time. And we’re living longer.

In 2011 in the U.S., Baby Boomers (people born from 1946 to 1964) began to reach the age 65 milepost marker. The Census Bureau estimates that the percentage of the population aged 65 and over among the total population will reach 20.9 percent by 2050. This group of older consumers will also be much more ethnically and racially diverse.

Speculation on how the Boomer generation is likely to reshape the American experience of aging has been lively. As with everything else they have touched, many have long surmised that Boomers are likely to transform the imagery, lifestyle and experience of old age in ways Americans are just now beginning to comprehend. So, younger generations, take notice because one day you will be the aging consumers.

Because older age groups will be outpacing the growth rate of younger age groups (and an elderly population will become the American majority for a sizeable share of the 21stcentury) the social and economic implications of an aging population should be of significant interest to food and beverage industry marketers. We’d suggest that this might be the right time to revisit these darlings of yesteryear and get to know what health and wellness means to them today.

Understanding Today’s Aging Consumers: Healthy Living And Adventures With Food

The new 50-and-older segment will eat, shop and live differently than today's 50-plus segment. Food and beverage distinctions like fresh, less processed, local and real will drive this new aging consumer with an underlying current of health and wellness impacting lifestyle choices. Such changes signal that approaches to aging are shifting, and marketing to new aging consumers requires a holistic point of view.

There has been, perhaps, no more pervasive lifestyle shift in the American contemporary scene than the desire among Baby Boomers to lead active, healthy lives. Although the pursuit of healthy living is not unique to Boomers, it is the initiative taken by aging Boomers to create a new way of living based on the pursuit of not just wellbeing but being well that has driven permanent changes in America food culture and healthy living.

To better understand the shape of these trends and the permutations for different segments of the marketplace, it is helpful to look carefully at Boomer and Silent consumers and their everyday strategies for living healthy, staying active and being well.

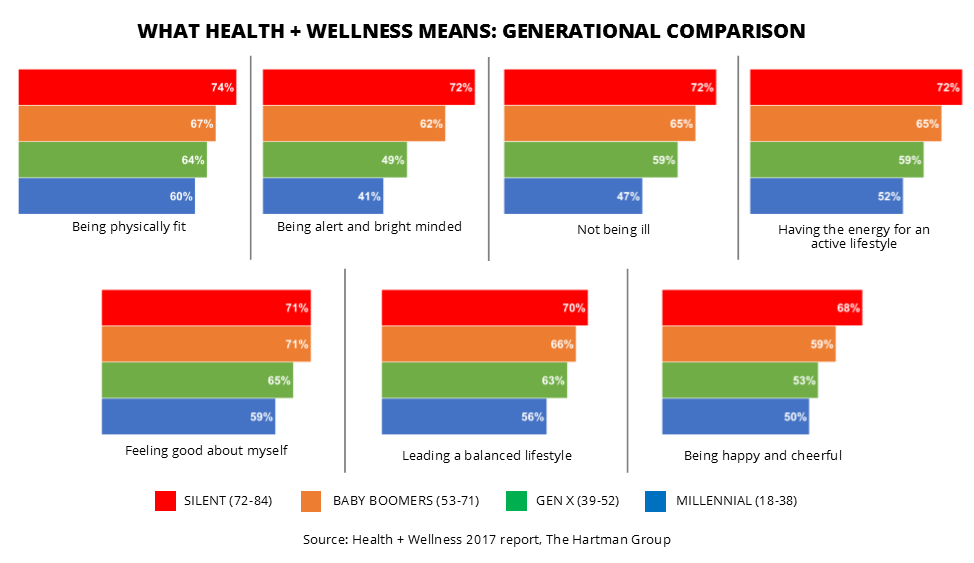

Here’s a snapshot look at the top seven attributes of what health and wellness means to consumers across the generational segments. Consumers continue to view health and wellness holistically, as maintaining balance in physical health, mental health, and lifestyle. Older consumers are more likely to think of health and wellness more broadly than younger consumers, likely reflecting the larger role it may play in their lives.

Engaging in and building habits they believe to be “healthy” allows consumers to enact “feeling well.” More than ever, consumers see interconnections between various components of their bodies, their habits, and the worlds in which they live. In particular, the connection consumers see between their physical and mental health is deepening. When one area of life is out of balance, it can cause a cascade of effects throughout their life.

Our Health + Wellness 2017 report finds that all generations share a similar vision of how wellness feels. Wellness is the feeling of when aspirations and actions come into happy alignment –without force, without discomfort, and without conflict with other desires. But the generations differ on how one actually achieves the feeling of wellness as depicted in the following chart on wellness strategies.

Spotlight on Silent Generation

In our previous years’ health and wellness reports, our sample has included ages 18-79, but for Health + Wellness 2017 we increased the age range to 18-84. This meant we could include a readable sample of Silent Generation consumers (defined as ages 72-84).

Silent Generation consumers are not what we would consider “trend forward” or “more engaged”health and wellness consumers, in that they have the highest percentage of lesser-involved Outer Mid-Level and Periphery consumers across our four generational cohorts. In this way, they aren’t that different from Boomers, but they are quite different from Millennials: 21 percent of Millennials are Periphery, whereas 30 percent of Silents are Periphery — the highest percentage.

Though overall Periphery consumers tend to be least engaged with health and wellness, the Silent Generation is very much engaged, but in much more “traditional,” mainstream ways. They have a broader definition of health and wellness than younger generations, going beyond physical health and good looks to encompass relaxation, feeling positive about oneself, and enjoying time with loved ones. This likely reflects their greater life experience — one can still aspire to wellness even if one’s physical condition is not what it used to be.

At the same time, Silents have a relatively static view of health and wellness — they are much less likely to have changed their views recently compared to all other age groups.

Silents are also in relatively good health — though the conditions they manage reflect their age, overall they treat and prevent approximately the same number of conditions as other generations.

One secret to the Silent generation’s longevity may lie in their BMIs. They are the least likely of all age cohorts to be obese, and most likely to have a normal BMI. Looking across age groups, overweight and obesity tend to increase with age up to a point, with both hitting their highest percentages among Boomers and older Gen X and dropping significantly after age 70. We can’t tell from our data whether Silents have better weight management strategies and health habits than Boomers or whether Silents who were overweight/obese succumbed to earlier deaths, but we suspect it is a mixture of both. In either case, they should serve as both a warning to and role model for the Boomers, who have the highest BMIs of all the generations, and are more likely to suffer from related conditions.

Older generations, and Silents in particular, are more traditional in other ways. They trust more than younger consumers do in “traditional” health authorities — doctors and the government — and less in alternative health practitioners, self-styled experts, and social circles. They don’t buy into contemporary health and wellness attributes, like organic (33 percent vs 51 percent of the general pop) or even ingredients they recognize (54 percent vs 65 percent of the general pop). They stick to traditional health advice (avoiding fat, salt, excess sugar, processed meats, and full fat dairy) at much higher rates than others. They add mainstream “good” ingredients — vitamin D, fiber, fish oil, whole grains, nuts and seeds, and olive oil. But they aren’t taken with trendy foods like coconut oil or chia seeds. They’re also happy to get good ingredients in supplement form, and while they are highly like to take vitamins and other supplements, they are much less likely to use botanicals and herbs, which corresponds to their traditional views on health and wellness.

Connecting with Older Consumers

As older consumers continue to look for ways to better themselves or improve the quality of their lives, they will affect the food and beverage industry in new ways. Time is becoming increasingly important to them, which translates into more conscious planning and more careful choices that express their values and aspirations. This aging population has many options from which to choose and they are looking for more than just a particular retailer, restaurant, product or service. They want their purchase to count: to satisfy mental, emotional and even spiritual needs as well. They are willing to be adventurous and experiment, which opens many doors for the food companies that cater to them.

No comments:

Post a Comment